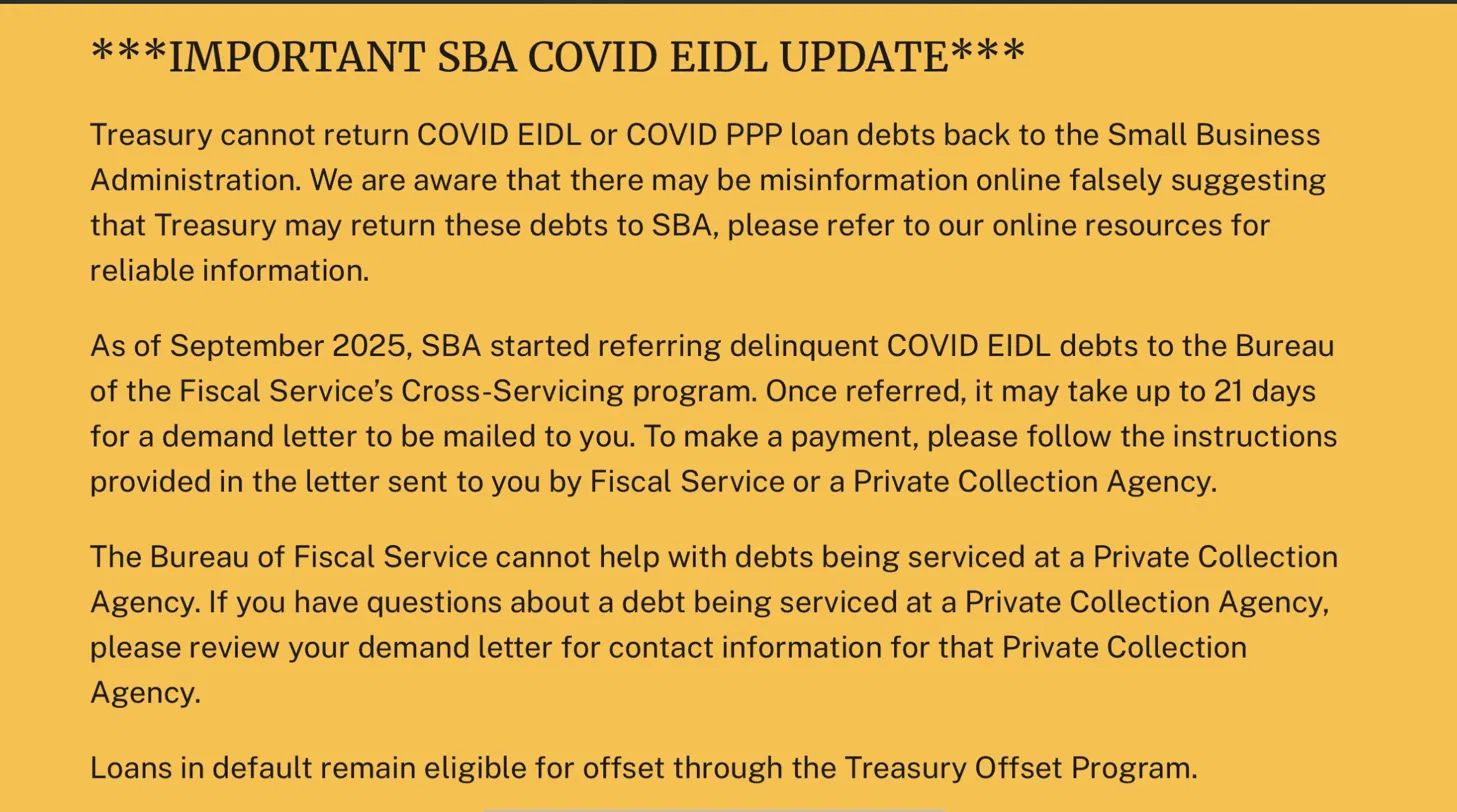

Treasury says it can’t return your COVID EIDL.Is that true?Yes. And no.

The Bureau of the Fiscal Service has a notice on its website stating it cannot return COVID EIDL or PPP debts to the SBA. Read it carefully. It answers one narrow question and stays quiet on the one that actually matters to a borrower.

A borrower cannot simply write to Treasury and say, “I want to be returned to the SBA, because…” Those odds are slim to none. Treasury’s published guidance is correct on its face: it will not return COVID EIDL or PPP debts to SBA at the borrower’s request.

Many borrowers hear the word “recall” and assume they can ask Treasury to send the debt back. That is where the confusion lives. A request to recall is not the same thing as the right to dispute the debt, challenge the referral, and ask the agencies to verify the account.

True as written. The notice speaks only to borrower-requested returns. It is silent on a borrower’s ability to dispute the debt, request validation, and ask the agencies to confirm the balance, the fees, and whether the referral was even done properly.

Forget forcing a recall. Ask whether the referral was done right.

The short answer: a borrower generally does not have a legal right to force a COVID EIDL debt to be recalled from Treasury Cross-Servicing. The more useful question is whether the borrower can dispute the debt, challenge the referral, request account reconciliation, and ask the agencies to review the account. The answer to that is yes, and the knowledge of whether the process was followed correctly sits with the borrower.

Asking Treasury to simply send the debt back to SBA because you want it back. There is no general borrower right to compel it, and Treasury’s own notice says it will not do it on request.

You are not necessarily arguing the debt does not exist. You are asking the agencies to verify that the balance is accurate, that the referral was proper, and that required procedures were followed before the debt was sent to Cross-Servicing. A dispute and a recall request are completely different instruments.

A dispute asks a question. A recall demand makes one. Questions get reviewed.

Six things you can put in writing.

Instead of demanding the debt be returned, a borrower may ask the creditor agency and Treasury to produce and confirm the record behind it.

SBA’s disaster loan servicing guidance, SOP 50 52 2, governs many aspects of disaster loan servicing and liquidation. Treasury’s Cross-Servicing procedures (TFM) govern collection activity after referral. Neither source hands borrowers a clear right to compel a recall, which is exactly why the factual review path is the one that tends to move.

The framework that governs these requests.

Read TFM Chapter 5000 →The strongest requests are built on records, timelines, payment history, and correspondence, not generalized demands for the debt to be returned.SmallBiz Recon · Field Doctrine

As a practical matter, borrowers tend to have more success focusing on factual review, documentation, account reconciliation, servicing history, and debt validation than on arguing an absolute right to force a recall. Specific questions backed by the account record carry weight. Generalized demands rarely do.

There’s a lot more in the full guide.

SmallBiz Recon™, a smarter approach to SBA COVID EIDL servicing document support. The complete Treasury referral guide breaks down the process, the paperwork, and how borrowers build a clean administrative record.